ONE would think that Asian equity markets would be happy at the news that China’s economy, the regional powerhouse, is growing even faster than expected.

Roaring too fast for comfort

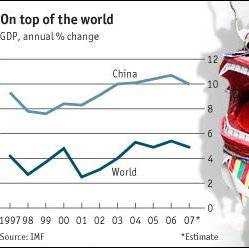

But that’s not the way it turned out. Shortly before China’s government said, late last week, that the economy grew at an annualised pace of 11.1% in the first three months of 2007, and as forecasts rose for the year’s overall growth, traders on the region’s big exchanges briefly took fright. The next day markets rebounded.

Nobody is jumpy about growth, of course, but of the government's reaction to it. Chinese officials are getting worried that a meltdown may be pending, and have been intervening to dampen things down. But over the past few years tighter interest rates, lending restrictions and heavier bank regulation have failed to cool the economy. Now they may have to be even more aggressive.

China’s fairly primitive financial infrastructure makes it difficult to fine-tune credit through monetary and fiscal policy. As worries grow about credit bubbles and overinvestment, no one knows quite how hard the government may need to step on the brakes. All this makes investors, who should be bullish, uncertain about what the near future may bring.

Across the Pacific, protectionists in America, who should be displeased to hear of even faster Chinese growth, may have found a note of cheer. If the Chinese government wants to get runaway growth under control, it may allow faster appreciation of the yuan.

Relations between China and America have been getting tense, thanks to the growing flow of cheap Chinese goods into American markets. But the Bush administration has so far stayed relatively friendly towards its trading partner. China has not been called a currency manipulator, despite domestic American pressure over the controlled currency. The yuan is now trading at about 7.7 to the dollar, up by a little over 7% since the Chinese currency went off its fixed peg in mid-2005. More vocal critics would like to see appreciation well into double digits, and have threatened sanctions if that does not happen. Until now, the administration has managed to stall such drastic moves with soothing talk about gradual increases.

That may be changing, however. China’s trade surplus with America and its foreign-exchange reserves continue to grow, making economists fidgety and protectionist politicians livid. In the first three months of this year alone, China added $135.7-billion worth of foreign currency to its reserves, compared with $247.3 billion for all of 2006. This coincides with the lame duck phase of the Bush administration, hamstrung by a newly Democratic congress, and politically crippled by the debacle in Iraq. With the 2008 presidential campaign getting into full swing, the administration is rapidly losing the will and strength to fight the protectionists.

On Friday April 20th Hank Paulson, America’s treasury secretary, said that Chinese officials “are not moving, in my judgment, quickly enough” to loosen restrictions on the yuan. In the past Mr Paulson has been rather sympathetic to the Chinese on their currency conundrum, so this does not bode well for relations between the two. Some now reckon that trade sanctions against China are on their way.

Indeed, they have already started. Last month, America slapped anti-dumping duties on imports of high-gloss paper from China, in response to a complaint from domestic manufacturers. It has also filed a complaint at the World Trade Organisation against Chinese copyright violations.

If the Chinese government were to let off some economic steam by allowing the yuan to appreciate more, this might—temporarily, at least—appease some of America’s “fair traders”. It also makes some economic sense for China. Because its financial infrastructure is a little shaky, the central bank is not completely able to “sterilise” its foreign-currency transactions. The massive reserves it is accumulating could therefore translate into inflationary pressure, forcing it to clamp down on growth. A more freely floating currency would ease this stop-and-go cycle.

However, it’s not clear how much impact this would really have on exports. For many of the products it exports, China is merely an assembler of parts made elsewhere, which is why its trade surplus with the rest of the world is less impressive than its bilateral one with America. Should the yuan rise, it will make those inputs cheaper for Chinese firms, so export prices will rise less than the yuan-bashers might hope.